Tokenised Gold and Commodities Guide 2026

An educational guide to tokenised gold in 2026 — PAXG and XAUT — covering how the backing chain actually works (vault, custodian, attestation or audit, token contract), the storage and redemption economics versus physical bullion and gold ETFs, the broader tokenised-commodities landscape (small but growing), and the portfolio role of tokenised gold relative to its alternatives. No partner CTAs; this page is about understanding the category before any action.

What Tokenised Gold Is in 2026

Tokenised gold is the most operationally mature category of tokenised commodities in 2026. Two products dominate the live market: PAXG (Paxos Gold), which sits at approximately $1.98B market cap against 456,894 PAXG circulating (CoinGecko live snapshot, June 2026), and XAUT (Tether Gold), which reported 707,747.139 fine troy ounces backing the token at a market value of $3.303B as of the 31 March 2026 BDO Italia attestation. Both tokens represent one troy ounce of allocated physical gold per token, both use LBMA-accredited vault custody, and both trade across most major centralised and decentralised exchanges with deep secondary liquidity.

The category sits in a meaningfully different position from the rest of the broader RWA market. Where tokenised treasuries compete with money-market funds and tokenised private credit competes with TradFi credit funds, tokenised gold competes with three distinct alternatives — physical bullion, gold ETFs, and other gold-exposure routes. The operational case is well-defined: lower annual carrying cost than a gold ETF, no 5-8% dealer-spread round-trip cost of physical bullion, 24/7 settlement, fractional units, and on-chain composability. The trade-offs are equally well-defined: counterparty risk at the issuer and custodian, the audit-versus-attestation distinction, and the jurisdictional perimeter that determines whether you can actually hold the token where you live.

This guide is structured around the operational mechanics rather than the price thesis. Whether or not gold belongs in a particular portfolio is a question this page does not try to answer; whether a reader who has already decided to hold gold should use the tokenised form is the question the rest of the page addresses. The mechanics matter because the integrity of the backing chain — vault, custodian, attestation, token contract — is the entire substance of what differentiates a credibly-backed tokenised commodity from a thinly-backed marketing exercise.

Two framing notes before we begin. First, this page is educational and carries no partner CTA. Readers who want the side-by-side product picker between PAXG and XAUT are routed to the dedicated head-to-head comparison guide, which covers each parameter at the granular level a product-selection conversation requires. Readers who want the operational access path — where to buy, which exchange, which wallet — are routed to the cluster's how-to-invest companion. Second, the XAUT figures throughout this guide use the Q1 2026 Tether attestation (31 March 2026 BDO Italia) as the single canonical source; do not mix these figures with the older CoinMarketCap snapshot that circulated in early 2026, because the issuer's own attestation is the authoritative number.

What Tokenised Gold Is

The shortest accurate definition is that tokenised gold is an on-chain token whose backing is a unit of allocated physical gold held in an LBMA-accredited vault. The token is the unit of ownership; the smart contract enforces transfer, minting, and burning; and the underlying bullion sits in the custodian's vault under terms documented in the issuer's offering materials.

One token, one troy ounce

Both PAXG and XAUT use the same denomination convention: one token represents one fine troy ounce of allocated gold. This matters because it makes the token's economic value mechanically tied to the spot gold price, less the issuer's published fees and the secondary-market basis. A holder of 5 PAXG holds a claim on 5 troy ounces of allocated gold; a holder of 10 XAUT holds a claim on 10 troy ounces. Fractional ownership of a single ounce is supported at the wallet level — the token contracts on both products support decimal precision, so a wallet can hold 0.25 PAXG or 0.10 XAUT just as easily as a whole-ounce position.

Distinction from gold-tracking synthetic tokens

A separate category of on-chain instruments — synthetic gold-price-tracking tokens — exists across various DeFi protocols. These instruments use derivative or oracle-based mechanics to track the gold price without holding allocated bullion as backing. They are not what this guide covers. The distinguishing test is whether the token represents a beneficial claim on physical gold held in a vault (PAXG, XAUT) versus a synthetic exposure to the gold price funded by collateral that is not itself gold (the synthetic category). The two routes have fundamentally different counterparty profiles, different regulatory framings, and different operational risks, and conflating them is a common first-time mistake.

Why tokenisation here works operationally

Gold is the commodity where tokenisation has worked most cleanly so far for three reasons. The asset is fungible and divisible in a way that simplifies the backing chain — one troy ounce of LBMA-accredited gold is operationally identical to any other troy ounce of LBMA-accredited gold. The vault-and-custody infrastructure pre-existed the on-chain wrapper, so the issuer is layering an on-chain mechanic on top of a mature TradFi process rather than inventing the whole stack. And the demand profile — investors who want gold-price exposure without personal possession of bullion — maps cleanly to what an on-chain wrapper actually delivers.

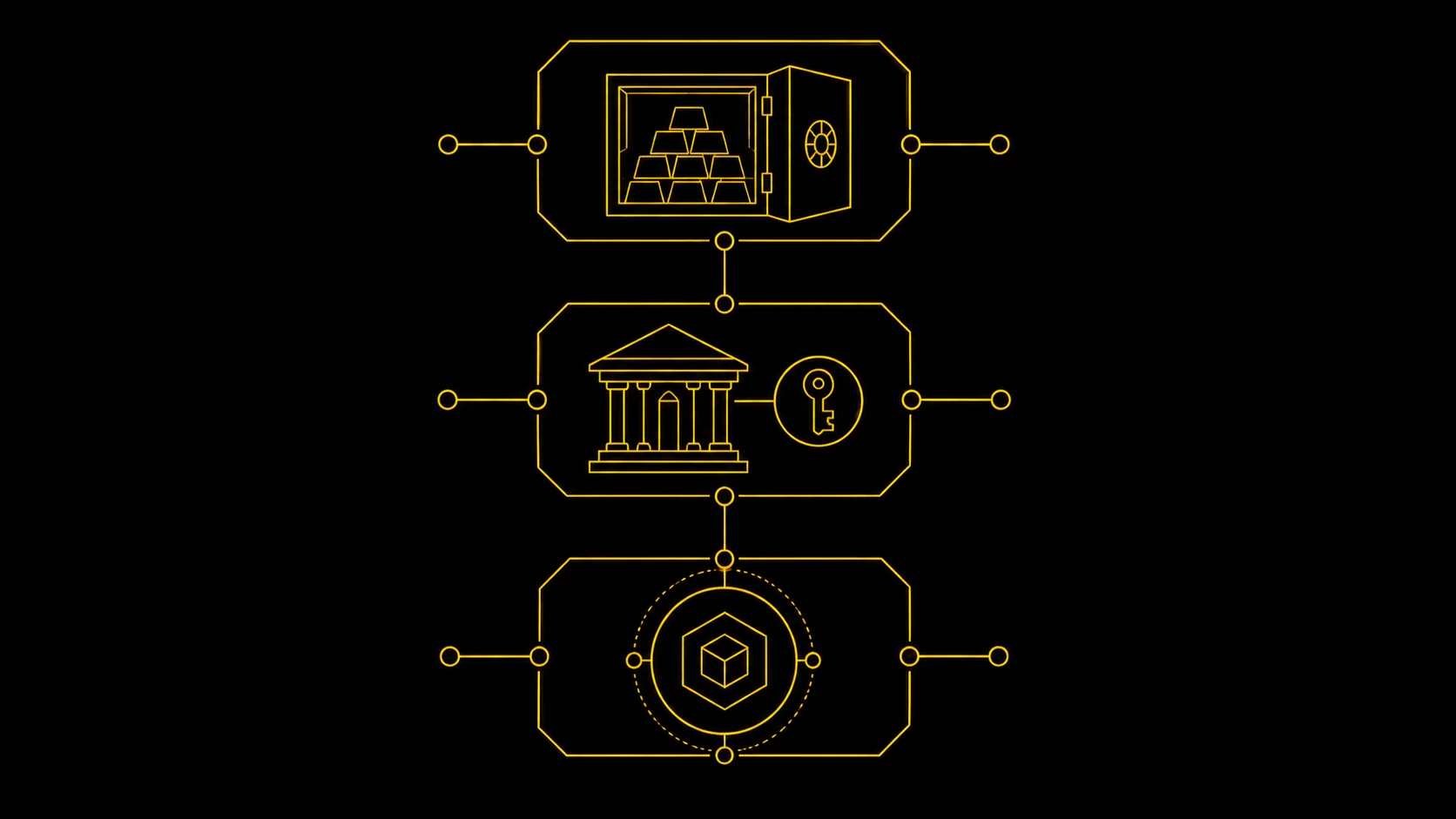

How Backing Works

The backing chain has four layers, each of which can be evaluated independently and each of which contributes a separate risk vector to the token's overall counterparty profile.

Layer 1 — the vault and physical bullion

At the base of the chain is allocated physical gold held in a vault. "Allocated" is a load-bearing term: it means that specific bars, identifiable by serial number, are earmarked against specific token supply, rather than the issuer holding an unallocated pool of bullion that could in principle be claimed by multiple parties. For both PAXG and XAUT, the underlying gold meets the LBMA Good Delivery standard — the London Bullion Market Association's bar specifications for institutional bullion, which establish weight, purity, and traceability requirements that have anchored the global wholesale gold market for decades.

Layer 2 — the regulated custodian

The custodian is the entity operating the vault and the legal counterparty to the issuer. For PAXG, the custodian operates LBMA-accredited vault facilities under Paxos's contracted arrangement, with Brink's having been the historic operator for the storage relationship. For XAUT, the custodial arrangement is Swiss-vault-based, with the custodian operating under the LBMA Good Delivery framework. The custodian is the single most important counterparty in the chain — if the vault operator fails or the bullion is misappropriated at the custody layer, the on-chain token's claim has no upstream resort.

Layer 3 — the attestation or audit

The attestation or audit is what links the on-chain token supply to the off-chain bullion holding. The mechanic and the cadence differ materially between the two products, and the difference is one of the most informative single signals about the category.

PAXG publishes monthly third-party attestations issued by KPMG LLP (since 28 February 2025; previously WithumSmith+Brown PC) that list bar serial numbers and vault locations, allowing a holder to verify that specific bars are allocated against the published token supply. The attestation cadence (monthly) and the level of detail (serial-level granularity) put PAXG at the top of the transparency hierarchy across the tokenised-RWA universe.

XAUT publishes quarterly attestations conducted by BDO Italia, with the most recent attestation as of this guide's draft date being the Q1 2026 review on 31 March 2026, documenting 707,747.139 fine troy ounces backing XAUT in circulation at a market value of $3.303B — approximately 36% expansion in fine troy ounces backing over Q1 2026 (520,089 → 707,747 oz). Note that the market value declined from approximately $4B at Q4 2025 to $3.303B at Q1 2026 as gold spot retraced, so the supply growth and the market-value figure move in different directions over the same window.

BDO Italia provides quarterly point-in-time attestation of reserves, not a full audit; Tether has indicated that audit engagement is in progress as part of preparations for US market entry. This distinction matters: a point-in-time attestation confirms balances on a specific date; a full audit examines the broader internal controls, reconciliation processes, and operational integrity that surround the balances. Both have value, and neither is a substitute for the other. Honest framing of the XAUT backing has to name the attestation-versus-audit distinction explicitly.

Layer 4 — the on-chain token contract

The token contract is the smart-contract code that mints, transfers, and burns tokens against the verified holding. Both PAXG and XAUT use ERC-20 tokens on Ethereum as the primary chain, with cross-chain wrappers available on selected additional chains. The contract logic is straightforward: a mint increases circulating supply when the issuer confirms a corresponding bullion allocation; a burn decreases circulating supply when a token is redeemed against the underlying bullion or for fiat. Transfer is unrestricted in the standard ERC-20 sense, which is what gives tokenised gold its composability and deep secondary-market liquidity profile.

Reading the backing chain for any tokenised commodity

The four-layer framework above applies to any tokenised commodity, not just gold. When evaluating a new tokenised-commodity product, the questions worth asking are the same questions you would ask of PAXG or XAUT, in the same order:

- What is the underlying physical specification (purity, weight, traceability) and which standard does it meet?

- Who operates the vault, and what regulatory regime governs the custodian?

- What attestation or audit cadence applies, and is it a point-in-time attestation or a full audit?

- What is the token-contract jurisdiction and regulatory framing, including transfer restrictions and redemption mechanics?

A product that gets clean answers on all four layers is a credible tokenised-commodity wrapper; a product that ducks one or two of them is signalling a backing chain that is structurally weaker than the leading tokenised-gold products.

Per-Product Overview

The two leading tokenised-gold products are profiled below in prose. The head-to-head side-by-side comparison — backing standard by parameter, custody location by jurisdiction, fee schedule by line item, redemption threshold by bar size — lives on the dedicated PAXG vs XAUT comparison page rather than being duplicated here. This page covers the mechanics and portfolio role; the comparison page owns the product-selection picker.

PAXG (Paxos Gold)

PAXG is issued by Paxos Trust Company, an OCC-regulated national trust as of 12 December 2025 (previously a New York Department of Financial Services (NYDFS) limited-purpose trust). As of June 2026, PAXG sits at approximately $1.98B market cap against 456,894 PAXG circulating, per CoinGecko live snapshot; the January 2026 24-hour trading volume exceeded $600M across major exchanges that list it after a record monthly inflow (CoinDesk, 28 January 2026), with trailing-30-day averages materially lower per CoinGecko. Circulating supply tracks allocated bullion held in LBMA-accredited London vaults (historically operated by Brink's as the custody partner). The product launched in 2019, making it one of the longest-running operational tokenised-gold issuances in the live market.

PAXG's transparency posture is the strongest single feature of the product. Monthly third-party attestations document the bar serial numbers, vault locations, and total allocated tonnage against the published token supply. A holder who wants to verify the backing chain can do so against the published attestation document each month, and the granularity of the disclosure means that an external party can mechanically check the supply-versus-backing equation. The NYDFS regulatory footprint adds a second layer of operational scrutiny on top of the attestation cadence, and the OCC oversight establishes a federal-level supervisory relationship that is unusual for a crypto-asset issuer.

On the redemption side, PAXG offers retail-tier redemption into fiat at most consumer-facing settlement venues. Physical-bar redemption is more constrained: it requires accumulating one full London Good Delivery bar (430 PAXG, currently around $1.2M+ at 2026 spot), delivery is to UK-approved vault facilities only, with fees in the $18-28k range and a 20-45 business-day timeline (per Paxos help docs and third-party redemption guides). The combination of retail fiat redemption, deep CEX and DEX listing depth, and the OCC-regulated issuer profile makes PAXG the default starting point for retail investors entering the tokenised-gold category in 2026.

XAUT (Tether Gold)

TG Commodities, S.A. de C.V. (El Salvador; relocated from BVI in January 2025; registered Stablecoin Issuer and Digital Asset Service Provider under El Salvador's Digital Asset Issuance Law) is the issuer of XAUT, operating under the Tether group umbrella with vault custody located in Switzerland (per Tether's own disclosure; no independent third-party Swiss custodian publicly named) under the LBMA Good Delivery standard.

The product's most recent published attestation — conducted by BDO Italia and dated 31 March 2026 — sets the backing at 707,747.139 fine troy ounces of allocated gold against tokens in circulation, equating to roughly $3.303B in market value, representing approximately a 36% expansion in fine troy ounces backing over Q1 2026 alone (note: the market value itself declined from ~$4B at Q4 2025 to $3.303B at Q1 2026 as gold spot retraced, so the ounce-supply growth and the market-value figure move in different directions over the same window).

The ounce-supply growth has made XAUT the larger product by total backing value at the close of Q1, even though PAXG continues to lead on operational track record and on the depth of the retail-fiat redemption channel that its counterpart does not yet match at retail scale.

XAUT's attestation framework merits explicit attention. BDO Italia provides quarterly point-in-time attestation of reserves, not a full audit; Tether has indicated that audit engagement is in progress as part of preparations for US market entry. This is not a fatal weakness — point-in-time attestation by a recognised firm is a meaningful disclosure layer, and the LBMA Good Delivery standard on the underlying bullion is independent of the attestation framework. But it is a structural difference from PAXG's monthly serial-level attestation, and any honest evaluation of XAUT should name the distinction rather than treat the two products' transparency postures as equivalent.

On the redemption side, XAUT physical redemption is structured around the bar sizes used in the underlying vault, with minimums consistent with the LBMA Good Delivery standard. The redemption mechanic is calibrated for large-position holders rather than retail-size positions seeking physical-bar delivery; for retail-size holders, secondary-market exit on a CEX or DEX is the operationally simpler path. The combination of substantial total backing value, broad exchange listing depth, and the LBMA Good Delivery standard on the underlying bullion makes XAUT a credible alternative to PAXG for investors comfortable with the quarterly attestation cadence.

Beyond Gold: Commodities On-Chain

Tokenisation of non-gold commodities is the structurally interesting frontier of the broader commodity-tokenisation conversation, but as of mid-2026 it is also the operationally thinnest. The category encompasses tokenised silver, oil-exposure tokens, and a handful of other commodity-tracking products, with each sub-category at a different stage of operational maturity.

Tokenised silver has the most direct claim to extending the gold model — the underlying physical specification is well-defined, the vault-and-custody infrastructure exists, and the LBMA-equivalent standard (the London Platinum and Palladium Market for the precious-metals sister markets, plus the silver-specific frameworks) provides the institutional bullion baseline. But no tokenised-silver product has yet approached PAXG or XAUT in AUM, liquidity, or attestation depth, and the market remains thin in 2026.

Tokenised oil exposure presents a fundamentally different structural problem because oil is not as fungible-and-divisible at the institutional level as gold. The standard market mechanism for oil exposure — futures contracts on specific delivery dates and grades — does not translate cleanly into a token-with-allocated-physical-backing model, and the tokens that exist in this category often use synthetic or futures-rolled mechanics rather than direct physical backing. Investors who want oil exposure are typically better served by ETF and futures routes until a credible physical-backed token emerges.

Other tokenised commodities — including small experimental products tracking carbon credits, diamonds, and various agricultural commodities — exist in 2026 but at a scale that does not approach the leading tokenised-gold products. The honest read is that the category beyond gold is structurally interesting but operationally immature, and the four-layer backing-chain test above is the right framework for evaluating any specific non-gold product. Specific product names in this sub-category move quickly and any recommendation would date faster than this guide can update; readers who want commodity exposure outside gold are typically better served by traditional ETF and futures routes until the tokenised non-gold products develop the operational depth that the leading tokenised-gold products demonstrate.

Tokenised silver — where the market currently is

The most-watched tokenised-silver experiments have come from boutique bullion-token issuers and from occasional Tether-affiliated XAG-pegged proposals over the post-2022 period. None has yet approached PAXG or XAUT in any of AUM, secondary-market depth, or attestation cadence. The reasons are structural rather than product-specific. Silver's industrial-versus-investment demand mix means the bullion supply chain serves industrial buyers (electronics, solar, medical) alongside investment buyers, and the LBMA-equivalent good-delivery standard for silver is less universally honoured by industrial supply contracts than the gold standard is.

Storage economics also differ — silver is a meaningfully bulkier metal per dollar of value than gold (silver in the roughly $30/ounce range in 2026 against gold's roughly $2,000/ounce range), which means a vault holding a given dollar value of silver requires roughly 60-70x the physical volume of an equivalent gold vault. Vault-level economics compound the issuer's storage costs, and the on-chain token has to either pass those costs through (annual storage fee) or absorb them (lower issuer margin), neither of which has been successfully scaled to PAXG-like depth.

The practical read for a 2026 investor curious about tokenised silver is that the category is investible at small position size for readers who specifically want the silver-price exposure, but the operational profile is materially thinner than tokenised gold and the same four-layer backing test introduced earlier in this guide should be applied with extra scepticism. A reader who would not size a position in physical silver because the round-trip cost is prohibitive is unlikely to find the tokenised-silver wrapper improves the situation materially in 2026; the cost case for tokenised gold against physical bullion does not replicate cleanly to silver yet.

Oil and energy tokens — why the model breaks

Tokenising oil exposure is structurally harder than tokenising precious metals because oil is not the same kind of asset at the institutional level. Spot oil is a continuous-delivery contract, not a divisible-and-storable physical good — there is no equivalent of "one troy ounce of allocated oil" that a vault can custody. Institutional oil exposure runs through futures contracts, with specific delivery dates, grades (Brent vs WTI vs Dubai), and delivery points. A tokenised-oil product can attempt to track oil prices through a futures-rolled mechanic (which carries roll cost during contango and roll yield during backwardation, and does not behave like spot oil over a multi-year holding window) or through a synthetic mechanic (which carries counterparty risk at the synthetic issuer without delivering physical exposure).

Neither route produces an instrument that behaves like the "tokenised gold model" extended to oil. For investors who want oil exposure as a portfolio diversifier, the cleanest 2026 routes remain energy ETFs (the major oil-tracking funds), the broader commodities ETFs, and direct futures positions for sized capital. Tokenised-oil products in 2026 are conceptually interesting but structurally incomplete, and the right framing for a retail reader is to treat them as not-yet-mature rather than as a smaller version of the tokenised-gold opportunity.

Carbon credits, agricultural commodities, and the experimental tail

The further fringe of commodity tokenisation includes carbon credits (Toucan and KlimaDAO are the most-cited examples from earlier waves, with continuing 2026 experiments around verified offsets and methodology-specific tokens), tokenised agricultural commodities (rare experimental products tracking grain, coffee, and other softs), and tokenised industrial metals (copper, platinum, palladium). Each carries category-specific structural challenges.

Carbon credits depend on the underlying verification standard's credibility — a token is only as good as the methodology that mints the underlying credit, and the credibility of various methodologies has been contested over the post-2022 period. Agricultural commodities face the same physical-fungibility problem as oil (a wheat token cannot be backed by "one bushel of allocated wheat" the way PAXG is backed by allocated gold, because wheat is delivered seasonally with specific grade and origin terms). Industrial metals are closer to gold structurally but commercially smaller; the platinum and palladium markets exist at a scale that supports institutional bullion infrastructure but not yet a tokenised-product market with measurable AUM.

The honest read of the experimental tail is that almost every product worth naming has either a narrow specific use case (carbon credits for corporate sustainability programmes, for example) or operational depth that does not yet match the leading tokenised-gold benchmarks. For readers who want commodity exposure as a portfolio diversifier in 2026, the practical sequencing is to start with tokenised gold (the operationally cleanest entry point). Evaluate gold ETFs and physical bullion as comparators on the cost and use-case dimensions. Treat the non-gold tokenised commodities as a watch-list category rather than an immediate allocation.

Applying the four-layer test to any tokenised commodity

The four-layer backing chain introduced earlier in this guide generalises beyond gold and gives a reader the framework for evaluating any commodity-tokenisation claim, including products that do not yet exist in 2026 but may emerge in subsequent quarters. Layer 1 — the physical asset: verify that the underlying commodity actually exists in a quantity matching the issuer's claim, in a form (allocated bars, contracted barrels, or whatever the unit is) that the issuer can identify specifically rather than generically. Layer 2 — the custodian: verify that a regulated entity in a credible jurisdiction holds the physical asset on behalf of the token issuer, with insurance and oversight appropriate to the asset class.

Layer 3 — the attestation or audit: verify that a recognised third party verifies the existence of the underlying asset on a cadence the issuer publishes, with the distinction between attestation and full audit named explicitly. Layer 4 — the token contract: verify that the on-chain contract behaves as the issuer describes, with the allowlist and freeze functionality named transparently rather than discovered after a transfer fails.

A tokenised commodity that fails any of the four layers is not necessarily a bad product, but it is not yet a "tokenised gold model" extended to a new asset class. The mid-2026 honest read is that gold is the only commodity where all four layers operate at retail-investible depth, and the rest of the category is at varying degrees of partial maturity. Readers willing to engage with that picture honestly are better served than readers chasing the marketing-narrative that "tokenised commodities" is a coherent category in 2026.

One closing framing note on the broader commodity-tokenisation thesis. The structural case for tokenised gold is anchored to the physical characteristics of the underlying metal — divisible, fungible, storable, and historically priced as a monetary good rather than primarily as an industrial input. Those characteristics do not generalise cleanly to silver (industrial demand mix dominates), to oil (futures-rolled exposure does not match spot price over a multi-year window), or to most agricultural commodities (seasonal delivery and grade variation break fungibility).

Investors who internalise that asymmetry will evaluate any future tokenised-commodity product against the specific structural fit of its underlying asset, rather than against the generic "tokenised commodities are the next category" pitch that has not yet produced an operationally mature non-gold product at the scale the leading tokenised-gold products demonstrate today.

Storage Fees and Redemption Mechanics

The annual-cost economics of tokenised gold are one of the cleanest single arguments for the category relative to its alternatives. The cost stack splits between holder-side fees (paid by the token holder for storage) and transaction-side costs (paid at acquisition, transfer, or redemption).

Holder-side fees

Both leading tokenised-gold products carry no annual storage fee at the token-holder level in 2026. PAXG explicitly absorbs storage costs into the issuer's operating model, with no per-holder annual storage charge; XAUT similarly carries no on-chain transfer fee and no annual storage fee at the token level. Verify the current fee schedule on each issuer's product page before sizing a position — fee structures do change — but the mid-2026 baseline is no holder-side annual fee for either product.

The contrast with gold ETFs is the most informative comparison point. SPDR Gold Shares (GLD) has historically charged approximately 0.40% per year as the expense ratio against fund net assets, deducted continuously as a reduction in the fund's daily NAV strike. iShares Gold Trust (IAU) has charged approximately 0.25% per year. For a $10,000 position held over five years, the cumulative cost differential between a no-fee tokenised-gold product and a 0.40% gold ETF is roughly $200, which is meaningful for cost-sensitive long-term holdings. The tokenised-gold path is the lower-annual-cost route, full stop.

Acquisition and redemption costs

Acquisition costs at retail size are driven by the secondary-market spread on the CEX or DEX where the buyer transacts, plus any gas cost for an on-chain transfer at the destination wallet. Both costs are minor at retail position size — typical CEX spreads on PAXG and XAUT are a fraction of a percent, and gas on Ethereum mainnet for a standard ERC-20 transfer is single-digit dollars at mid-2026 conditions. For positions in the $1,000-$50,000 range, the all-in acquisition cost is well under 1% of the position value.

Compare to physical retail bullion, where retail dealer spreads typically run 5-8% over spot at purchase, with a similar spread (or wider, depending on bar size and condition) on the sale side. A round-trip on physical bullion at retail size frequently costs 10-15% of the position value, even before accounting for storage and insurance for held bullion. For a buyer whose use case is gold-price exposure rather than personal possession of bullion, the tokenised-gold cost structure is materially better.

Redemption costs depend on the destination. PAXG retail fiat redemption routes through the supported settlement venues; the cost is the spread or fee at the venue, plus any wire-transfer cost on the fiat receive leg. PAXG physical redemption requires one full London Good Delivery bar (430 PAXG, currently around $1.2M+ at 2026 spot), delivery to UK-approved vault facilities only, fees in the $18-28k range, and a 20-45 business-day timeline (per Paxos help docs and third-party redemption guides). XAUT physical redemption follows the LBMA Good Delivery standard's bar-size conventions, which means retail-size holders are typically better served by secondary-market exit rather than direct physical redemption.

Portfolio Role

For an investor who has already decided gold belongs in their portfolio, the choice between physical bullion, a gold ETF, and tokenised gold turns on use case rather than on the gold-price thesis itself. A worked example with three identical $10,000 allocations makes the trade-offs concrete.

$10,000 in physical bullion

The buyer pays roughly $10,500-$10,800 at acquisition (5-8% retail premium over the $10,000 spot value of the metal), receives physical bars or coins, and stores the holding personally or at a paid storage facility. Annual storage cost ranges from zero (home storage) to approximately $50-150 (third-party safe-deposit or precious-metals depository), depending on the holder's preference and risk tolerance. Resale runs through a retail dealer at a similar 5-8% spread, so a hypothetical round-trip at the same spot price recovers roughly $9,200-9,500 of the original $10,000 — a 5-8% structural cost regardless of price movement. This is the right path for an investor whose use case explicitly requires personal possession of bullion; it is structurally costly for an investor whose use case is gold-price exposure.

$10,000 in a gold ETF

The buyer pays roughly $10,005-$10,010 at acquisition (typical brokerage spread plus any commission), receives shares of the ETF (GLD or IAU being the most common at retail size), and pays an annual expense ratio of 0.25-0.40% against fund NAV. For a $10,000 holding over five years at a 0.40% expense ratio, the cumulative cost is approximately $200; at 0.25%, approximately $125. Sale runs through the brokerage at similar small spreads, so the round-trip cost at the same spot price is approximately 0.5-1% all-in, plus the annual expense ratio. This is the right path for an investor whose flows live entirely in a brokerage account and who values the regulatory familiarity of a US-registered ETF wrapper.

$10,000 in tokenised gold

The buyer pays roughly $10,025-$10,075 at acquisition (CEX or DEX spread plus gas), receives PAXG or XAUT in their self-custody wallet (a hardware wallet such as Ledger is the standard recommendation for position sizes that materially affect savings), and pays no annual storage fee. Cross-border transferability and 24/7 settlement come built-in; the position is composable with the rest of an on-chain portfolio for any downstream use. Sale runs through the same CEX or DEX with the same small spread, so the round-trip cost at the same spot price is approximately 0.5-1.5% all-in, with no annual carrying cost.

This is the right path for an investor whose use case is gold-price exposure on rails compatible with the rest of an on-chain portfolio, who accepts counterparty risk at the issuer and custodian, and who is comfortable with the attestation-versus-audit distinction (especially for XAUT).

The three trade-offs that distinguish the routes

The decision between the three routes reduces to three trade-offs, in roughly this order of importance:

- Personal possession. Physical bullion is the only route that delivers personal possession. If that is the use case, neither ETF nor tokenised gold substitutes.

- Regulatory familiarity. A US-registered ETF wrapper carries the most familiar regulatory profile for investors whose other holdings live in a brokerage. Tokenised gold carries a different but operationally credible profile (NYDFS for PAXG; Swiss vault custody and BDO Italia attestation for XAUT). Physical bullion carries no regulatory wrapper beyond the consumer-protection rules of the dealer's jurisdiction.

- On-chain composability. Tokenised gold is the only route that delivers on-chain composability — usable as collateral, swap-pair, or yield-strategy input within the constraints of the token's allowlist behaviour. ETF shares are useless for any on-chain use; physical bullion is even further removed.

For readers ready to take operational steps on the tokenised-gold path — which exchange to use, which wallet to put the token in, which chain to settle on — the cluster's how to invest in RWA guide covers the access path at the operational level.

Conclusion

Tokenised gold in 2026 is the most operationally mature category of tokenised commodities, anchored by two products — PAXG (~$1.98B market cap against 456,894 PAXG circulating per CoinGecko live snapshot, June 2026) and XAUT (707,747.139 fine troy ounces of backing, $3.303B market value as of 31 March 2026) — that share the one-token-one-troy-ounce convention and the LBMA-accredited vault custody baseline while differing on attestation cadence, regulator, and redemption mechanics. The category is a credible alternative to physical bullion and gold ETFs for investors whose use case is gold-price exposure on rails compatible with the rest of an on-chain portfolio.

The annual-cost economics favour tokenised gold against ETFs (zero holder-side fee versus 0.25-0.40% expense ratios); the round-trip cost economics favour tokenised gold against retail physical bullion (under 1% versus 10-15% dealer-spread round-trip). The trade-offs are counterparty risk at the issuer and custodian, the audit-versus-attestation distinction (PAXG monthly serial-level attestations; XAUT quarterly BDO Italia point-in-time, with full audit engagement in progress), and the jurisdictional perimeter that varies by product and by holder's location. For investors who want personal possession of bullion, no tokenised wrapper substitutes; for investors who want regulatory familiarity above all else, gold ETFs continue to be the institutionally familiar choice; for everyone else who already operates on-chain, tokenised gold is the operationally cleanest of the three.

For the side-by-side product picker between PAXG and XAUT — backing standard by parameter, custody location, fee schedule, redemption threshold, and exchange-listing depth — the dedicated PAXG-vs-XAUT comparison page in Related Articles below is the next read. For the operational step-by-step on actually buying PAXG or XAUT in a self-custody wallet, the cluster's how-to-invest companion handles the access path. The broader RWA cluster hub maps tokenised gold against the other three RWA categories for readers who want to put gold in context with treasuries, private credit, and real estate.

Sources and References

Live market-cap, attestation, and fee figures change quickly. Verify each figure against the primary source — typically the issuer's own product or attestation page — before sizing a position.

- Tether Gold (XAUT) product page and Q1 2026 attestation — 707,747.139 fine troy ounces, $3.303B market value as of 31 March 2026 (BDO Italia point-in-time attestation)

- Paxos Gold (PAXG) product page — OCC-regulated national trust (converted from NYDFS on 12 December 2025), LBMA-accredited London vault custody, monthly third-party attestations issued by KPMG LLP since 28 February 2025 (previously WithumSmith+Brown PC), with bar serial numbers and vault locations

- LBMA Good Delivery standard — institutional bullion specifications underlying both PAXG and XAUT custody

- SPDR Gold Shares (GLD) prospectus — historical 0.40% per annum expense ratio reference

- iShares Gold Trust (IAU) prospectus — historical 0.25% per annum expense ratio reference

- New York Department of Financial Services (NYDFS) — primary regulator for Paxos Trust Company, the PAXG issuer

- Office of the Comptroller of the Currency (OCC) — federal oversight layer applicable to Paxos Trust Company

Disclaimer: Tokenised commodities carry significant risk, including total loss of capital. This guide is for educational purposes only and does not constitute financial, legal, or tax advice. Market-cap, attestation, fee, and redemption-mechanic figures are point-in-time references; verify against the primary source before making allocation decisions. Always consult a qualified professional for advice specific to your jurisdiction.

Frequently Asked Questions

- What is tokenised gold in 2026?

- Tokenised gold is an on-chain token whose backing is a unit (one troy ounce in both PAXG and XAUT) of allocated physical gold held in an LBMA-accredited vault. The token transfers, settles, and (subject to issuer mechanics) redeems on a blockchain; the underlying bullion sits in a regulated custodian's vault, with periodic attestations linking the on-chain supply to the off-chain holding. PAXG (Paxos Gold) sits at approximately $1.98B market cap against 456,894 PAXG circulating, per CoinGecko live snapshot as of June 2026; XAUT (Tether Gold) reported 707,747.139 fine troy ounces backing the token at a market value of $3.303B as of the 31 March 2026 BDO Italia attestation.

- How is tokenised gold backed?

- The backing chain has four layers: a physical vault holding allocated bars; a regulated custodian operating the vault; an attestation or audit confirming the on-chain token supply matches the holding; and the token contract that mints, transfers, and burns against the verified holding. PAXG uses Paxos Trust Company (OCC-regulated national trust since 12 December 2025; previously NYDFS limited-purpose trust) and LBMA-accredited vaults, publishing monthly third-party attestations issued by KPMG LLP since 28 February 2025 (previously WithumSmith+Brown PC) that list bar serial numbers and vault locations. XAUT uses Swiss vault custody under the LBMA Good Delivery standard, with BDO Italia publishing quarterly point-in-time attestations; Tether has indicated that audit engagement is in progress as part of preparations for US market entry.

- What is the difference between PAXG and XAUT?

- Both PAXG (Paxos Gold) and XAUT (Tether Gold) represent one troy ounce of allocated physical gold per token, but they differ on regulator, vault location, attestation cadence, redemption mechanics, and operational track record. PAXG sits under OCC-regulated Paxos Trust Co (since 12 December 2025; previously NYDFS limited-purpose trust), uses LBMA-accredited London vaults (Brink's as the historic operator), publishes monthly third-party attestations issued by KPMG LLP (since 28 February 2025; previously WithumSmith+Brown PC) with bar serial numbers, and offers retail fiat redemption alongside physical redemption. XAUT uses Swiss vault custody, publishes quarterly BDO Italia point-in-time attestations, and physical redemption requires bar-size minimums consistent with LBMA Good Delivery. The head-to-head comparison covers each parameter in detail.

- What are the storage fees on tokenised gold?

- PAXG carries no holder-side storage fee — Paxos absorbs storage costs as part of the issuer's operating model. XAUT carries no on-chain transfer fee and no annual storage fee at the token level. Compared to gold ETFs — GLD has historically charged around 0.40% per year, IAU around 0.25% per year — tokenised gold is materially cheaper to hold on an annual basis. Physical retail bullion typically trades at a 5-8% premium over spot at purchase, which is recovered (or not) at sale through the dealer spread; tokenised gold avoids that round-trip cost for buyers who do not need physical possession.

- Can I redeem tokenised gold for physical bars?

- Both PAXG and XAUT support physical redemption, with mechanics that differ in detail. PAXG retail-tier redemption is into fiat at most consumer-facing settlement venues; physical redemption requires accumulating one full London Good Delivery bar (430 PAXG, currently around $1.2M+ at 2026 spot), delivery to UK-approved vault facilities only, with fees in the $18-28k range and a 20-45 business-day timeline (per Paxos help docs and third-party redemption guides). XAUT physical redemption is structured around the LBMA Good Delivery standard, with minimums consistent with the bar sizes used in the underlying vault. Verify the current minimums and the supported delivery jurisdictions on the issuer's product page before sizing a position that depends on physical redemption.

- Is tokenised gold a real substitute for physical gold?

- For investors whose use case is exposure to the gold price rather than personal possession of bullion, tokenised gold is operationally cleaner than physical bullion and meaningfully cheaper than a gold ETF on an annual-fee basis. The trade-offs are counterparty risk (the issuer and the custodian both have to honour the claim), the audit-vs-attestation distinction (especially for XAUT, where the quarterly BDO Italia review is a point-in-time attestation rather than a full audit), and the regulatory perimeter (US accessibility for XAUT is in transition; PAXG sits under NYDFS regulation but state-by-state availability still applies). For investors whose use case explicitly requires personal possession of bullion, tokenised gold is not a substitute.

- Are tokenised commodities beyond gold worth holding?

- Tokenised silver, tokenised oil exposure, and a small number of other commodity-tracking tokens exist in mid-2026, but the market remains thin with no single non-gold product approaching PAXG or XAUT in AUM, liquidity, or attestation depth. The honest read is that the category beyond gold is structurally interesting but operationally immature. Readers who want commodity exposure outside gold are better served by traditional ETF and futures routes until the tokenised non-gold products develop the operational depth that the leading tokenised-gold products demonstrate.

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.